We compiled these trends from over 100 brands, comparing year-over-year data for the date range May 1, 2026, to May 31, 2026.

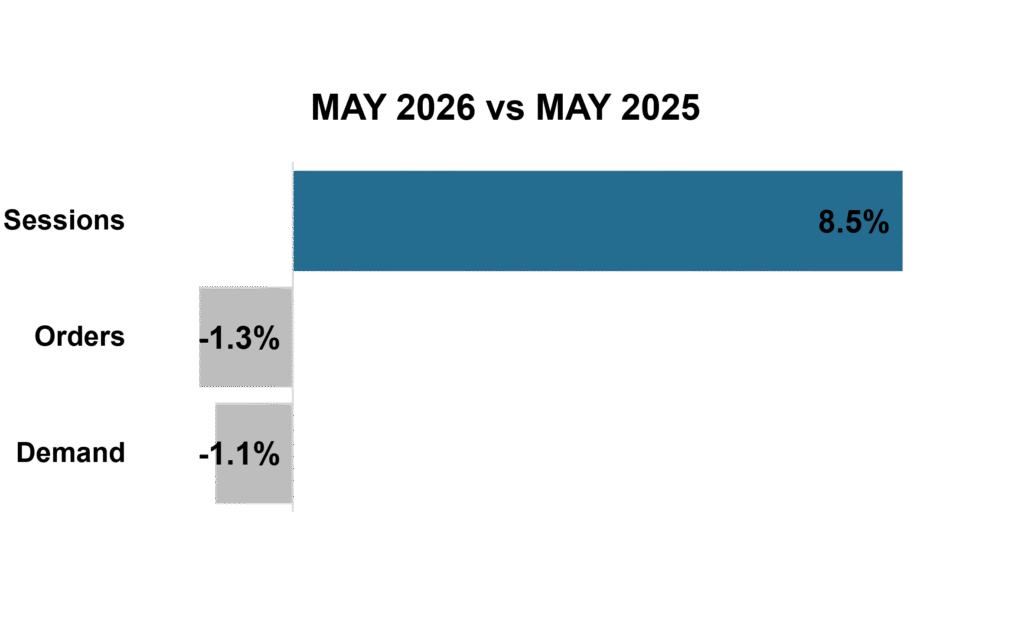

May 2026: Traffic Outpaced Orders as Shoppers Prioritized Value

May showed that consumers remain engaged. Sessions increased more than 8%, but that growth did not translate into orders. Orders and demand declined 1.3% and 1.1%, respectively.

Conversion held steady in apparel and home, while outdoor and specialty retailers experienced year-over-year declines. Average order value remained close to last year, though some brands are seeing pressure on basket size. Across categories, consumers remain thoughtful and value-conscious.

Higher food and fuel costs continue to influence discretionary spending. Households are actively managing finances, with the savings rate declining to around 2.6%. This suggests consumers are largely maintaining their lifestyles rather than making sharp cutbacks.

Overall sentiment remains measured, but demand is steady. Economic indicators point to slower yet stable growth. Consumers are cautious but still active in the market.

May 2026 Marketing Trends

Trend #1: How Smart Mailers Will Respond to Upcoming Postage Increase (PI World)

The USPS has proposed another postage increase set to take effect in July 2026, and for many marketers, the first reaction is predictable: “Should we mail less?” That’s the wrong question.

The better question is: “How do we make our mail work harder?” Despite rising postage costs, direct mail continues to outperform many digital channels in response, recall, engagement, and trust. The marketers seeing the best results today are not abandoning mail. They are becoming more strategic with it.

Poor strategy costs more than postage ever will. I’ve seen campaigns with mediocre targeting, weak creative, and generic offers waste thousands of dollars while highly targeted, well-designed mailings generate exceptional ROI, even at higher postage rates.

When direct mail is done correctly, it still commands attention in ways digital advertising often cannot. Consumers are overwhelmed online. Physical mail still has the ability to slow people down, create interaction, and build trust. That matters.

Read the Full Article: How Smart Mailers Will Respond to Upcoming Postage Increase

Trend #2: Brands are catching World Cup fever even without official sponsorships (Modern Retail)

From major splashy ad rollouts by Nike and Adidas to sponsorships by Anheuser-Busch and Coca-Cola, there is no shortage of brand collaborations for this summer’s FIFA World Cup.

But not all brands will pour millions of dollars into official sponsorships. Some smaller U.S. startups, like Crumbl Cookies and Olipop, are getting into the spirit of the World Cup with watch parties, soccer-themed products and more, taking advantage of their proximity to matches to get in on what will perhaps be the biggest cultural moment of the year. With millions of tourists descending on North America in the coming months, brand executives feel they have to find a way to capitalize on this moment.

According to a new Bank of America Global Research report, the 2026 World Cup is set to be the biggest to date, with 75% of the world set to engage with the event in some way. “Sectors best positioned to benefit from the World Cup include beverages, sportswear, restaurants, broadcasting, social media and online betting,” the report said.

Read the Full Article: Brands are catching World Cup fever without official sponsorships

Trend #3: How brands are celebrating 250 years of America amid political polarization (Retail Dive)

Last summer, a record-low 58% of U.S. adults said they were “extremely” or “very” proud to be an American, per a Gallup poll. That figure was down 9 points from the previous year and nearly 30 points from when the firm first polled Americans about their pride in January 2001. While Gallup has yet to reveal this year’s findings, 2026 so far has delivered month after month of political polarization and economic strain, taking a toll on consumers.

But even as the culture wars that have ensnared brands like Bud Light and Target continue — this time with a red, white and blue facade — there is still value in being associated with America. For example, Brand Keys’ 25th annual index of patriotic brands includes a top 10 featuring institutions like Coca-Cola, Ford, Disney, Amazon and Walmart — companies with big marketing footprints and bigger market values.

“As we gear up for the 250th party, more brands are viewed through a political lens — and authentic patriotism is more important than ever,” Robert Passikoff, president of research firm Brand Keys, said in a press release.

Read the Full Article: How brands are celebrating 250 years of America amid political polarization | Retail Dive

Trend #4: Retail sales grow again in May (Chain Store Age)

Consumers continue to show their resilience as retail sales rose for the eighth consecutive month in May despite high gas prices and ongoing inflation.

Total retail sales (including restaurants, but excluding automobile dealers and gasoline stations) increased 0.42% month over month and were up 7.19% year over year in May, according to the CNBC/NRF Retail Monitor released by the National Retail Federation. That compares with increases of 0.34% month over month and 5.73% year over year in April.

Read the Full Article: NRF: Retail sales grow again in May | Chain Store Age

Jump to Section

Marketing KPIs: May 2026 Trends by Industry

Marketing KPIs: May 2026 Trends by Company Revenue

$100M+ | $15M-$100M | $0-$15M

Marketing KPIs: May 2026 Trends by Industry

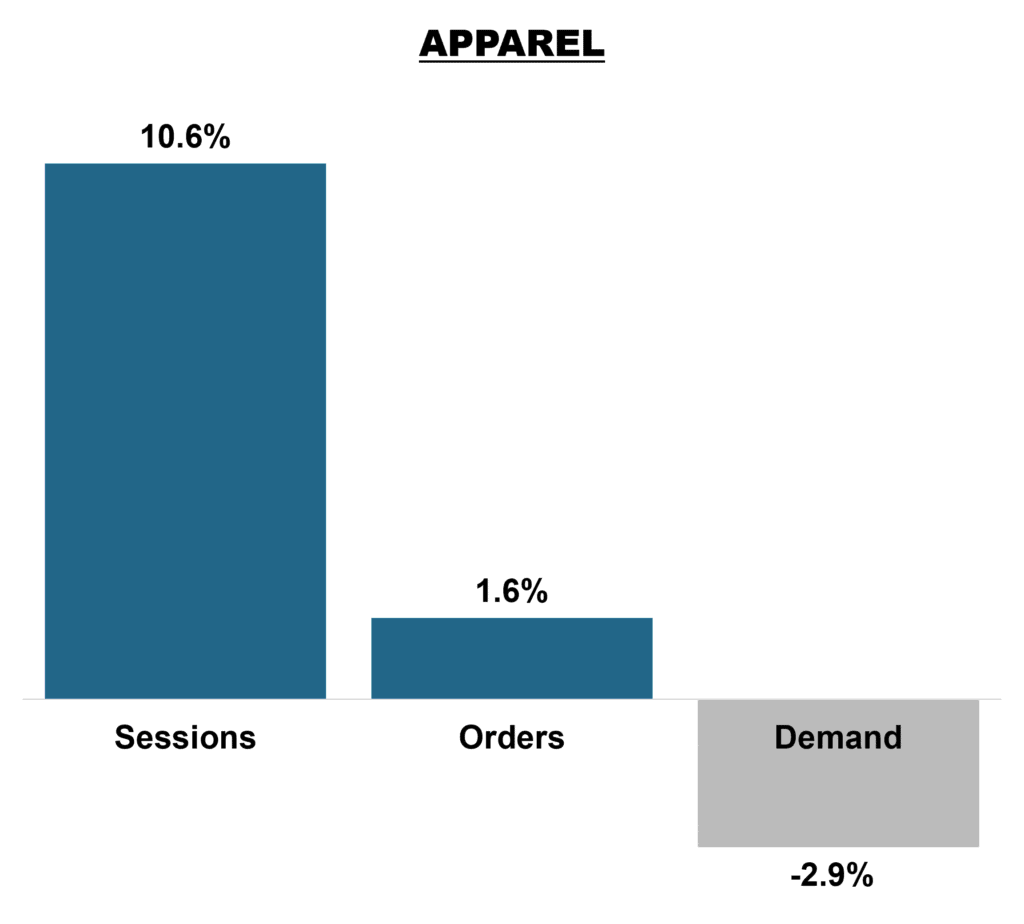

Apparel Brands

In May, sessions increased 10.6% year over year, signaling strong consumer interest in apparel. However, this traffic did not fully convert. Orders rose only 1.6%, while revenue declined 2.9% due to pressure on average order value and product mix.

Interest in apparel remains strong. The challenge is converting that interest into transactions and driving higher-value purchases.

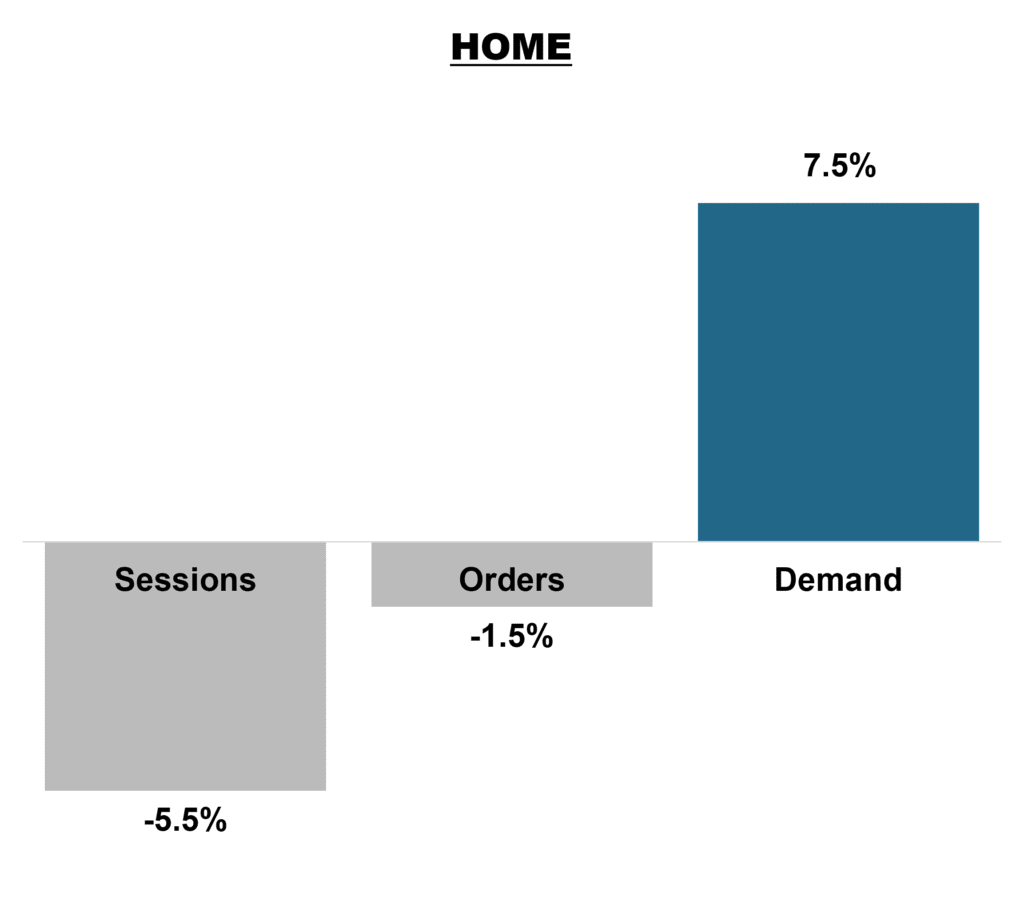

Home Brands

Home brands saw sessions decline 5.5% year over year in May, with orders down 1.5%. However, revenue grew by 7.5%, significantly outpacing traffic and orders, driven by higher average order values.

This suggests gains from pricing, premium product mix, or larger basket sizes, even as traffic remains under pressure.

In the near term, brands should focus on rebuilding traffic through targeted acquisition while preserving average order value through pricing, merchandising, and upsell strategies.

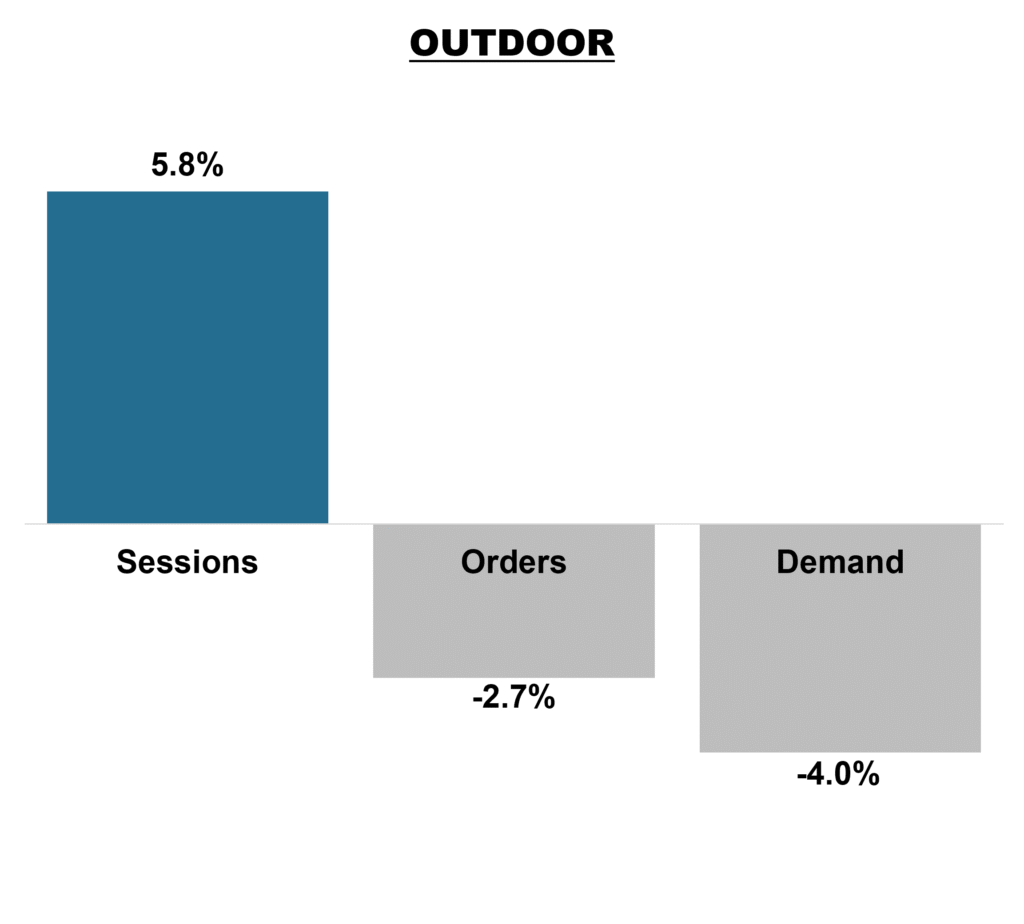

Outdoor Brands

Outdoor brands saw traffic growth in May, with sessions up 5.8% year over year. However, orders declined 2.7%, indicating the additional traffic did not convert. Demand fell 4.0%, suggesting pressure on average order value and a shift toward lower-priced products.

Weather variability has disrupted seasonal patterns in some regions. Increased competition and promotions have also made shoppers more price sensitive and slower to convert.

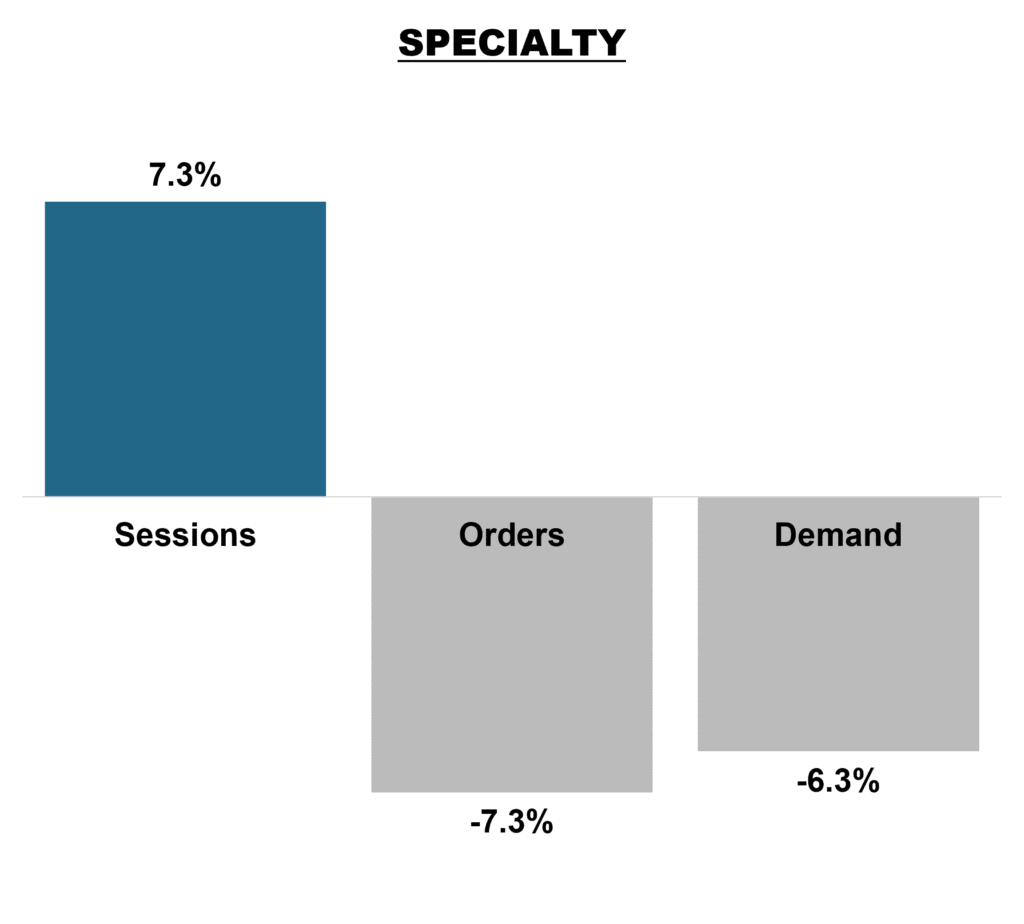

Specialty Brands

Specialty brands saw strong traffic in May, with sessions up 7.3% year over year. However, orders declined 7.3% as traffic failed to convert. Revenue fell 6.3%.

Specialty products are often discretionary, making them more vulnerable when consumers become price sensitive or uncertain. Customers continue to browse and engage but are more likely to delay purchases or choose lower-priced alternatives.

Marketing KPIs: May 2026 Trends by Company Revenue

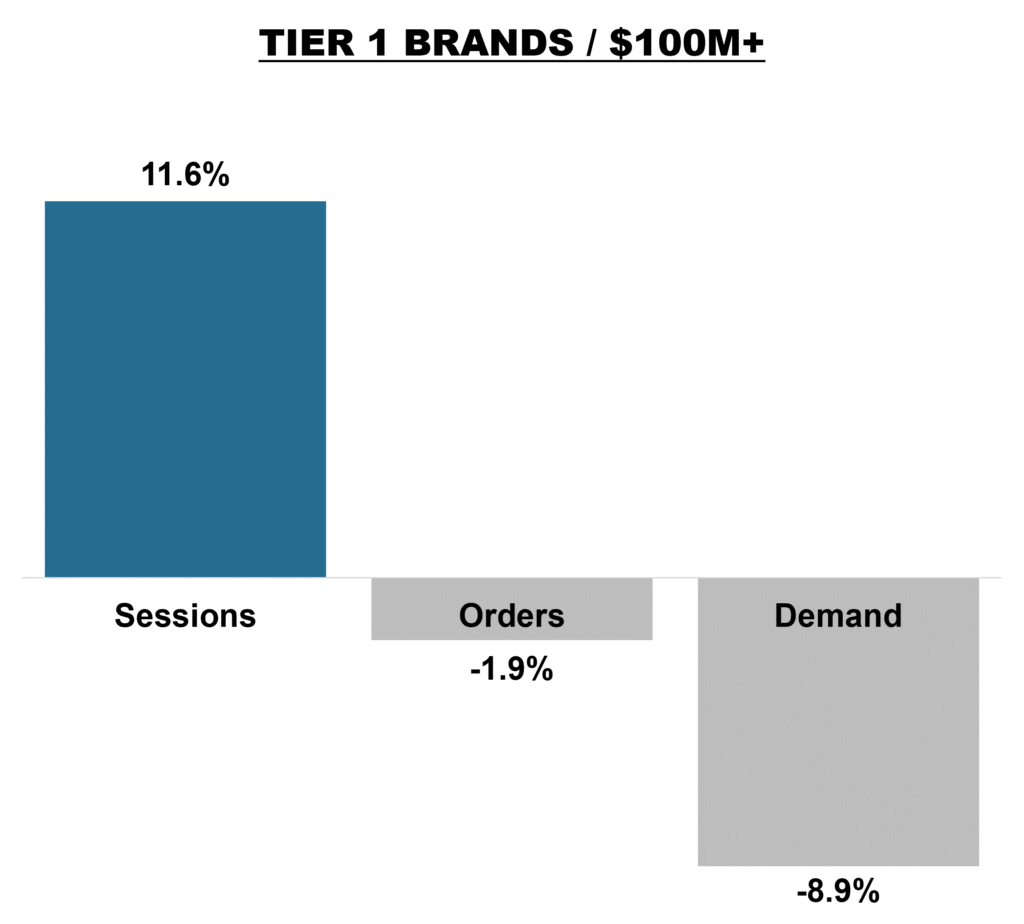

Tier 1 Brands

Sessions increased 11.3% year over year for Tier 1 brands, showing strong engagement. However, orders declined 1.9% as traffic did not convert.

Revenue dropped 8.9%, indicating pressure on average order value and product mix. While top-of-funnel performance is strong, the challenge is converting that traffic into higher-value baskets and repeat purchases.

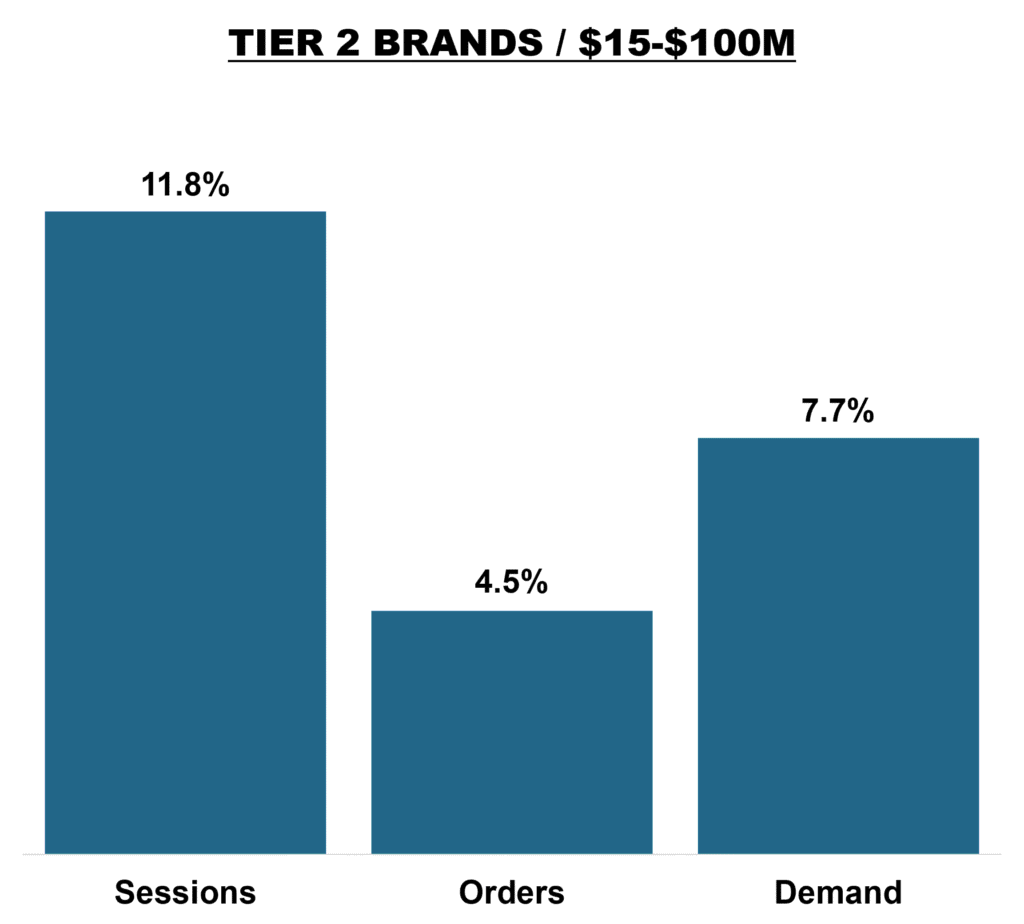

Tier 2 Brands

Tier 2 brands delivered strong performance in May. Sessions increased 11.8%, and orders rose 4.5%, reflecting healthy demand and stable conversion.

Revenue grew 7.7%, driven by higher average order value and favorable product mix. Growth remains balanced and efficient heading into summer.

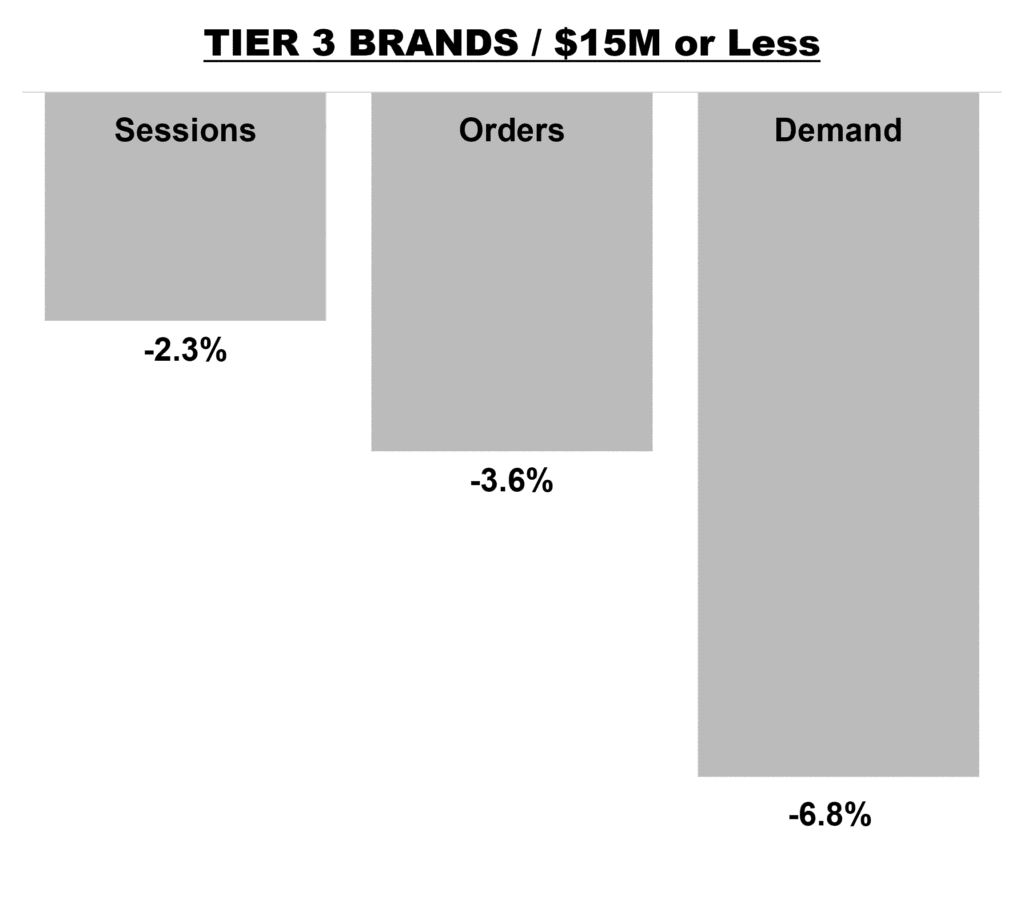

Tier 3 Brands

Smaller brands saw declines across key metrics in May. Sessions fell 2.3% year over year, orders declined 3.6%, and revenue dropped 6.8%.

The sharper revenue decline suggests customers are spending less even when they convert. Trade-down behavior and increased promotions are likely contributing factors. Narrow assortments can amplify this impact, as fewer items or lower-priced purchases quickly reduce revenue.

In the News

Print Isn’t Dead, It’s Getting More Interesting

For years, the loudest voices in marketing insisted that print was fading into irrelevance. But step back from the noise, and a different story emerges. Print isn’t dying, it’s evolving.

2026 Direct Mail Marketing Benchmark Report

The report also examines consumer sentiment, highlighting the sustained relevance of direct mail: 79% of consumers actively engage with mail, and 21% made a purchase in the past year as a result of receiving relevant content.

Read More →

Unlock the Power of Traditional Outreach in a Digital-First World

In an era dominated by screens and social feeds, businesses are rediscovering the power of print. Direct mail, long considered an old-school tactic, is proving to be a highly efficient, data-driven, and measurable channel in today’s marketing mix.

Read More →

Direct Mail Results & Statistics

Direct mail has an average response rate of 4.1%, exceeding email’s 1.7%.

61% of consumers have made a purchase after receiving direct mail.

Personalized direct mail offers boost response rates by 20% compared with generic ones.

Read More →

GET IN TOUCH

Questions? Need help integrating online and offline channels?

Tags: April 2026 Marketing Benchmarks, April 2026 Marketing KPIs, marketing, Strategy