We compiled these trends from over 100 brands, comparing year-over-year data for the date range September 1, 2024, to September 30, 2024.

September 2024: Consumers Remain Cautious

Consumers remained cautious in September. Traffic was up for many brands, however faced with persistent inflation and high borrowing costs, consumers continue to limit discretionary purchases. While some are still spending, the overall pace has slowed.

In an increasingly promotional environment, there are concerns about excessive discounting. Home and Outdoor brands faced the greatest challenges, last month. While Specialty retailers saw mixed results. Spending on Apparel continued, although growth was minimal. Even major brands are contending with reduced demand.

The impacts of Federal Reserve rate cuts is still uncertain. Analysts anticipate that rate cuts could encourage more spending, but the effects will take time to materialize. Economic data suggests that many consumers are in a more stable financial position, yet their spending intentions remain subdued. Brands that clearly articulate value may have a competitive edge as consumers become more intentional with their purchases.

September 2024 Marketing Trends

Trend #1: The Risk of Cutting Catalogs: Don’t Abandon Print in Favor of Digital

Retailers cutting back on catalog production in favor of digital marketing may face unintended consequences, including a significant drop in sales. For example, when Lands’ End reduced its catalog distribution in 2000, they saw a $100 million decrease in revenue. Orvis recently announced plans to discontinue its catalog, a decision that may negatively impact their sales, especially since many consumers have a strong emotional connection to print catalogs.

Despite the rise of digital marketing, catalogs remain a highly effective tool. Their tactile nature and nostalgic appeal create a unique customer experience that digital channels cannot replicate. Moreover, print catalogs can break through the clutter of digital advertising, offering consumers a more personal and engaging interaction with a brand.

Retailers who eliminate catalogs may also lose out on valuable consumer insights and disrupt established seasonal buying habits. Catalogs provide important data on customer behavior that digital tools alone may not fully capture. Additionally, many shoppers plan purchases around catalog releases, and without them, retailers risk missing out on these well-timed sales.

Rather than abandoning catalogs entirely, retailers should consider a hybrid approach. Companies like Amazon have successfully blended traditional and digital marketing by creating interactive experiences through printed catalogs. By integrating catalogs with online channels, retailers can maintain the benefits of print while leveraging digital tools to engage customers and drive sales.

Trend #2: Home Furnishing Retailers Struggle As Housing Market Weighs on Sales

Home furnishing retailers faced major challenges in Q3 2024, as rising mortgage rates and a sluggish housing market weakened consumer demand for big-ticket items like furniture and home improvement products. Major players, including Williams-Sonoma, Wayfair, and Home Depot, reported year-over-year sales declines, reflecting broader economic issues like affordability concerns, high borrowing costs, and inflation. These conditions have led consumers to delay or reduce home-related purchases.

Williams-Sonoma, owning brands like Pottery Barn and West Elm, saw revenue declines in Q3, with Pottery Barn struggling due to lower demand for high-end furnishings. Similarly, Wayfair, which targets more budget-conscious shoppers, experienced a modest revenue decrease despite earlier cost-cutting measures.

Home improvement retailers like Home Depot and Lowe’s also faced declines, especially in large discretionary projects like kitchen and bathroom remodels that depend on financing. High mortgage rates and reduced home sales have curbed demand for renovations, DIY products, and home maintenance items.

Although some regions show signs of stabilization, the outlook for home furnishings and improvement retailers remains uncertain. While inventory levels have improved and mortgage rates slightly decreased, a substantial sales rebound has yet to occur. Retailers may need to adopt new strategies, such as competitive pricing and focusing on smaller, affordable products, to attract consumers in the coming months.

Trend #3: eCommerce Giants Amazon, Wayfair Use Print to Drive Web Sales

Amazon has embraced physical catalogs for several years, sending its customers a full-sized edition of about 100 pages near the holidays. This initiative, which has been running for at least three years, shows Amazon’s commitment to engaging customers through physical media.

They’re also embracing another proven tactic by versioning the catalog covers based on the recipient’s purchase history, creating a more relevant shopping experience. Among our recipient group, we saw two distinct cover versions tailored to reflect individual interests and past purchases, a strategy that’s sure to drive strong responses.

It’s telling to see an ecommerce giant like Amazon recognize the potential of print in supplementing its online store. By sending out physical catalogs, they create a cross-channel marketing approach that bridges the gap between digital and traditional shopping experiences. This move acknowledges that many consumers still appreciate the tactile experience of flipping through pages and discovering new products in a curated format, something that is often lost in the digital realm.

Similarly, Wayfair, another major player in the online retail space, has also seen the value in expanding its use of print media rather than cutting back on it. Initially focusing on direct mail campaigns, Wayfair has taken progressive steps to integrate a full-sized catalog into its marketing strategy.

Trend #4: From Artificial to Authentic: Modern Consumers Can Spot a Fake

Savvy consumers are increasingly able to identify AI-generated content, noticing certain keywords like “delve” and “tapestry” that are often overused by AI. Although most still trust brands to use AI effectively, they expect marketers to apply it responsibly and authentically. While tools like ChatGPT initially impressed users with their capacity to generate large volumes of content quickly, many began to notice patterns that indicated a lack of genuine human touch.

As a result, brands now face the challenge of using AI without compromising authenticity. Instead of relying solely on automated text, companies are integrating AI strategically, such as using it to enhance personalization or improve customer insights while keeping the human element at the forefront.

Lacta’s “AI Love You” campaign used AI to generate personalized love letters, an approach that resonated with its customers and aligned with it’s lovey-dovey brand identity.

This shift focuses on leveraging AI to support authentic engagement and maintain a consistent brand voice, ensuring that technology serves to deepen rather than weaken customer trust. By aligning AI’s strengths with their own values, brands can create experiences that feel both innovative and genuine, maintaining customer connections even in a digital-first era.

Trend #5: AI is Reshaping Market Research with Synthetic Data, Predictive Analytics

Synthetic data is transforming market research by offering a way to generate artificial yet realistic datasets that mimic actual consumer behaviors. This approach helps address challenges like privacy concerns and limited real-world data, allowing researchers to extract insights without compromising sensitive information. The use of AI-generated synthetic data not only speeds up data collection but also enables companies to explore new market scenarios more freely.

AI also powers predictive analytics, making market trend forecasting more precise. It uses machine learning algorithms to analyze large data sets, identify patterns, and predict future consumer behaviors or market shifts. This helps businesses adjust strategies quickly in response to emerging trends, improving the accuracy of demand forecasting and customer segmentation.

Moreover, AI tools like natural language processing (NLP) are increasingly used to analyze unstructured data, such as customer reviews and social media content. This allows companies to gain deeper insights into consumer sentiment, preferences, and emerging needs without manual analysis. By automating these processes, AI reduces the time and costs associated with traditional market research while offering richer, more nuanced insights. These advances are shaping a more agile, data-driven approach to understanding markets and consumer behavior, ensuring that research keeps pace with the evolving digital landscape.

For more, you can read the full article here.

Jump to Section

Marketing KPIs: September 2024 Trends by Industry

Marketing KPIs: September 2024 Trends by Company Revenue

$100M+ | $15M-$100M | $0-$15M

Marketing KPIs: September 2024 Trends by Industry

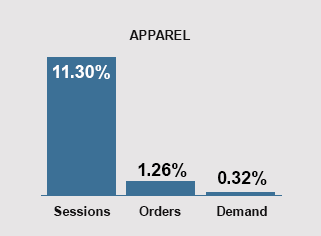

Apparel Industry

• Sessions Increased +11.30%: Apparel retailers continue to see increased sessions.

• Orders Increased +1.26%: While there was a noticeable increase in traffic, the rise in orders was much smaller.

• Demand Nearly Flat +0.32%: Consumers continue to spend at similar levels to last year. Even larger brands are experiencing demand challenges.

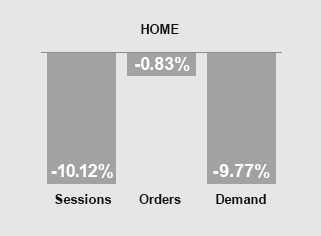

Home Brands

• Sessions Decreased -10.12%: Sessions for home retailers fell in September 2024 compared to last year, reflecting challenges from a cooling housing market and economic uncertainty.

• Orders Were Down -0.83%: The minimal decline in orders points to improved conversion. However, lower AOVs point to increased discounting.

• Demand Decreased -9.77%: Inflationary pressures have reduced disposable income, prompting consumers to cut back home goods along with other non-essential purchases.

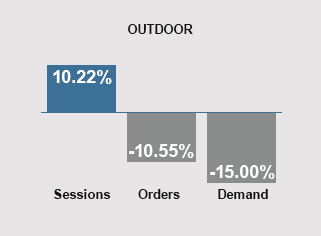

Outdoor Brands

• Sessions Increased +10.22%: Consumers continue to show interest in the outdoor space, however brands have struggled to capitalize on increased traffic.

• Orders Decreased -10.55%: The decline in orders for outdoor brands highlights ongoing conversion challenges. High inventory levels have led to heavy discounting, conditioning many outdoor consumers to expect lower prices.

• Demand Declined -15.00%: Demand declined by 15% as retailers increasingly offered discounts. Outdoor consumers are also shifting spending from products to experiences.

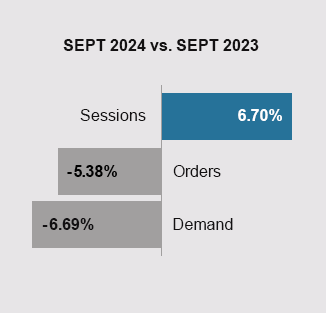

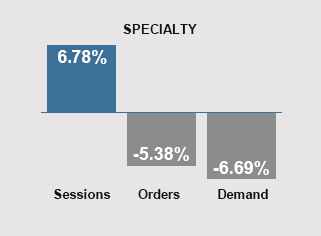

Specialty Retailers

• Sessions Increased +6.78%: Specialty Retailers saw increased sessions this September compared to the same month last year, reflecting growing consumer interest and engagement.

• Orders Decreased -5.38%: Orders fell in September, as consumer spending remains cautious. However, brands are hopeful that upcoming events, like Black Friday, might provide a boost.

• Demand Decreased -6.69%: The decline in demand further reflects a cautious consumer.

Marketing KPIs: September 2024 Trends by Company Revenue

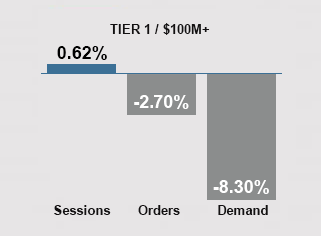

Tier 1 Brands

• Sessions Nearly Flat +0.62%: Session numbers for Tier 1 brands indicate stable engagement.

• Orders Decreased -2.70%: The decline in orders, highlights challenges in boosting conversions and maintaining Average Order Values (AOVs).

• Demand Declined -8.30%: A significant drop in demand suggests heavy discounting. Brands are increasingly turning to promotions to drive sales.

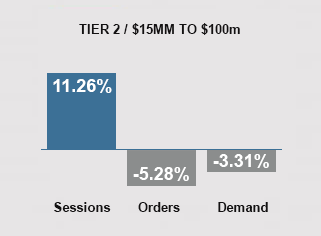

Tier 2 Brands

• Sessions Increased +11.26%: A rise in session volumes was observed among many Tier 2 brands, indicating stronger customer interest.

• Orders Decreased -5.28%: The decrease in orders suggests potential challenges in converting customer interest into sales.

• Demand Decreased -3.31%: Demand is softening across various sectors, particularly discretionary purchases This shift has prompted many brands to re-evaluate their pricing strategies and promotional strategies to emphasize value.

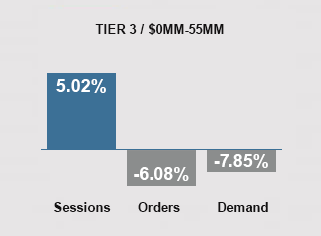

Tier 3 Brands

• Sessions Increased +5.02%: Tier 3 brands saw an improvement in sessions compared to September 2023. Interest in smaller, more niche brands appears to be growing.

• Orders Decreased -6.08%: Despite the growth in sessions, there was a decline in orders, suggesting a potential disconnect between traffic and conversion rates.

• Demand Declined -7.85%: The decline in demand aligns with broader economic trends, as consumers increasingly prioritize essential over discretionary spending.

In the News

USPS Announces No Postal Increase January 2025

The USPS announced that there will be no price changes in January 2025, maintaining current rates. This is a welcome announcement to many, after several recent increases.

Hurricane Service Alerts

This hurricane season has seen devastation in parts of the US. Stay informed on the latest USPS service disruptions due to hurricanes with this interactive map. It provides real-time updates on any closures or delays, ensuring you can plan accordingly for your mailing and shipping needs during severe weather.

Jerrell Lewis Promoted to Executive VP of CohereOne

Jerrell Lewis has been promoted to the position of Executive Vice President and General Manager at CohereOne. Her leadership will play a key role in enhancing CohereOne’s service offerings and expanding its market presence.

Case Study: Campaign Drives 28% YOY Sales

Pomegranate, a brand known for its vibrant hand-block print home textiles, wanted to bring a cohesive and unified brand message to all its marketing channels. They needed a way to integrate their storytelling and aesthetic seamlessly across print, email, social media, and web platforms, making sure they resonated with their audience no matter the season.

GET IN TOUCH

Questions? Need help integrating online and offline channels?

Tags: August 2024 Marketing Benchmarks, August 2024 Marketing KPIs