We compiled these trends from over 100 brands, comparing year-over-year data for the date range July 1, 2024, to July 31, 2024.

July 2024: Consumers Watch Their Wallets

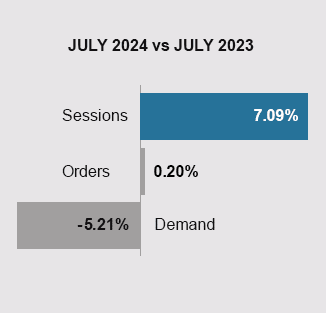

Consumers exhibited caution with their spending in July. Although there was an increase in sessions for many retailers, this did not translate into higher sales, with order volumes remaining flat. Overall, U.S. retail sales grew modestly by 0.74% month-over-month, indicating that while consumers continue to spend, they are doing so carefully. The July jobs report from the Bureau of Labor Statistics also painted a mixed picture of the U.S. labor market, further highlighting consumer restraint in discretionary spending.

Apparel and Outdoor brands outperformed many Home and Specialty retailers, buoyed by the back-to-school season and the Olympics, respectively. Nevertheless, demand appears constrained across verticals. In this challenging environment, refining strategies to enhance customer conversion rates and focus on improving customer lifetime value (LTV) will be crucial.

July 2024 Marketing Trends

Trend #1: Customer Retention and Reactivation with Direct Mail

Customer retention and reactivation are critical components of a successful business strategy, as retaining existing customers often yields a higher return on investment than acquiring new ones.

Brands frequently integrate these tactics through digital programs, often email. Combining direct mail with digital marketing efforts ensures a cohesive customer journey. For example, following up on a purchase with both a thank-you postcard and a personalized email can strengthen the customer relationship, encouraging future interactions.

Establishing loyalty programs is another effective strategy. By rewarding customers with exclusive offers, early access to new products, or points toward future purchases, businesses can encourage repeat purchases and long-term loyalty.

Specialized direct mail programs designed to deepen customer relationships, drive repeat purchases, and re-engage lapsed customers, are one of our most effective tactics from a ROAS perspective. Brands benefit from immediate improvements in conversion and increased lifetime value.

Trend #2: July Jobs Report / Economic Outlook

July’s Bureau of Labor Statistics (BLS) jobs report revealed a mixed picture for the U.S. labor market and overall economy. The economy added 114,000 nonfarm payroll jobs, significantly lower than the expected 175,000. The unemployment rate increased slightly to 4.3%, up from June’s 4.1%.

Growing Sectors

- Healthcare: +57,000 new jobs, a continuation of previous growth.

- Construction: +25,000 new jobs, likely driven by ongoing demand for housing and infrastructure projects.

- Transportation and warehousing: + 14,000 jobs, reflecting steady growth in logistics and delivery services.

Shrinking Sectors

- Information: -20,000 jobs, marking a significant contraction as companies in technology and media adjust to changing market conditions.

- Professional and business services: -1,000 jobs, which often include temporary help and management consulting.

Flat to Slow Growth

- Retail trade: +4,000 jobs, continues to struggle with the shift to e-commerce and changes in consumer behavior.

- Manufacturing: +1,000 jobs; indicating potential challenges in industrial production and global trade dynamics.

This mixed job market performance has implications for monetary policy. The Federal Reserve will likely scrutinize these numbers closely as it considers future interest rate adjustments in the coming months.

Trend #3: Exploring Sustainability from All Angles

There is a growing awareness of the environmental impact of the lifecycle of retail goods. It’s exploded regarding fast fashion, but ecological awareness is also increasing for home decor and other verticals as well. As consumers prioritize eco-friendly and sustainable products in their purchasing decisions, brands whose practices, merchandise and brand align with this trend may explore it from a few different angles.

1) Materials: Highlight sustainable materials, eco-friendly dyes, and production processes, or emphasize the use of sustainable materials, such as organic cotton, bamboo or recycled fibers. Example: Allbirds, Nothing New.

2) Processes: Highlight sustainable production processes that reduce carbon footprint and waste and showcase the use of eco-friendly dyes and techniques that minimize water and chemical usage.

3) Product lifecycle: Companies can reduce waste by making products that last and creating a forum for people to resell what they no longer want. Brands like Patagonia are taking stewardship of the product lifecycle in a whole new way. Example: Adidas’ Futureloop recyclable sneaker.

Read more: Forbes, Business Insider

Trend #4: Simplified, Value-Focused Messaging

In response to economic uncertainty, many retailers are simplifying their messaging to focus on value. This doesn’t necessarily mean low prices but rather the value proposition—durability, quality, and long-term benefits of the products.

Retailers are reducing the complexity of their offers, avoiding flashy discounts in favor of clear, honest pricing. This trend is also reflected in direct mail strategies, where smaller, more straightforward mailers with a focus on value are being used to offset rising postal costs.

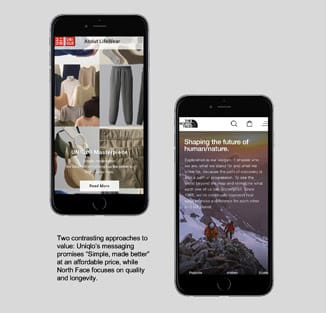

UNIQLO is known for its straightforward and value-focused messaging, emphasizing quality, functionality, and simplicity in its clothing. Their messaging often centers around providing “LifeWear”—clothing designed to be affordable, durable, and versatile for everyday use. The brand’s campaigns highlight the practicality and quality of their products, without relying complex messages.

Value-focused doesn’t always mean inexpensive, however. The North Face, while known for high-quality outdoor gear, has also focused on value in terms of durability and longevity of their products. Their messaging often underscores the idea that their gear is built to last, making it a valuable investment for outdoor enthusiasts.

Trend #5: Personalized and Hyper-Localized Marketing

Retailers are increasingly using personalized content that speaks directly to the consumer’s location, lifestyle, and preferences. Brands are leveraging data from loyalty programs, mobile apps, and purchase history to tailor promotions. This is especially effective in email marketing and direct mail campaigns, where personalized content can drive higher engagement and conversion rates.

We are all familiar with hyper-personalized experiences like the “just for you” content delivered based on your personal tastes and watch history from streaming platforms like Netflix and Spotify. In addition, product recommendation algorithms on websites show us product recommendations similar to items we are shopping for and have previously viewed.

Sephora’s use of personalized marketing is well-known through their Beauty Insider program. They use purchase history, location, and browsing behavior to send personalized product recommendations and exclusive offers.

Sephora has also run hyper-localized events and beauty classes in their stores, tailored to the preferences of customers in that area. For example, they might offer a specific skincare class in a city known for its harsh winter weather, focusing on products that cater to cold climates.

Read more: Idomoo

Jump to Section

Marketing KPIs: July 2024 Trends by Industry

Marketing KPIs: July 2024 Trends by Company Revenue

$100M+ | $15M-$100M | $0-$15M

Marketing KPIs: July 2024 Trends by Industry

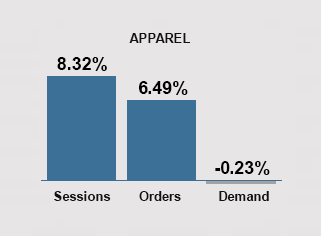

Apparel Industry

•Sessions Increased 8.32%: Consumers continue to actively shop for apparel, and brands continue to successfully drive traffic to their websites.

•Orders Increased 6.49%: Brands continue to improve conversion. Back-to-school shopping provided a lift, with a 5% increase in clothing and accessories spending. Brands also see increased sales through their mobile platforms.

•Demand Declined -0.23%: Despite more sessions and orders, the slight decline in overall demand likely signals increased price sensitivity. As consumers navigate financial pressures, they might be more selective with their purchases, focusing on essential or high-value items while reducing overall spending.

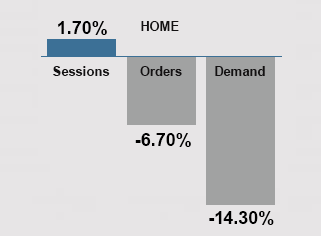

Home Brands

•Sessions Were Up 1.70%: A modest increase in sessions indicated a slight uptick in customer interest and engagement. However, this did not translate into positive outcomes.

•Orders Were Down -6.70%: Home brands continue to face conversion challenges. This parallels the real estate market, which has continued to cool.

•Demand Decreased -14.30%: The sharp decline in demand shows a significant decrease in consumer interest or willingness to spend on home and furniture products.

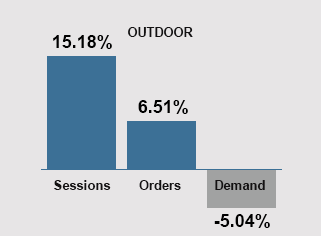

Outdoor Brands

•Sessions Increased 15.18%: The notable increase in sessions was fueled by the excitement of the Olympics and favorable July weather.

•Orders Were Up 6.51%: The increase in conversion rate roughly follows the rule of halves.

•Demand Declined -5.04%: Lower AOVs indicate increased price competition and deeper discounts.

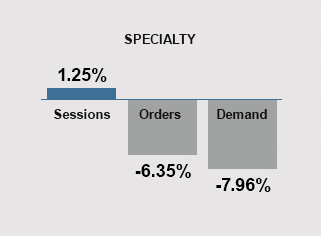

Specialty Retailers

•Sessions Increased 1.25%: Minimal YOY growth in sessions suggests interest in specialty goods is flat.

•Orders Decreased -6.35%: The decline in orders reflects consumers more conscious with their discretionary purchases.

•Demand Decreased -7.96%: Despite increased customer engagement, many consumers are exercising caution in their spending due to ongoing economic uncertainties.

Marketing KPIs: July 2024 Trends by Company Revenue

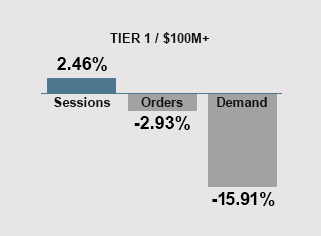

Tier 1 Brands

•Sessions Increased +2.46%: Tier 1 brands saw minimal growth in sessions compared to Tier 2 and Tier 3.

•Orders Decreased -2.93%: The modest decline in orders is magnified by the significant decrease in AOVs. In addition to conversion rates, brands may want to pay additional attention to items per transaction.

•Demand Declined -15.91%: Large declines in demand compared to last July point to heavy discounting.

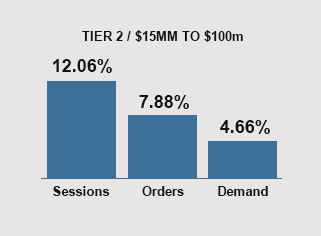

Tier 2 Brands

•Sessions Increased +12.06%: Many Tier 2 brands saw significant growth in sessions. Higher session volumes indicate that brands are successfully engaging potential customers and increasing brand awareness.

•Orders Increased +7.88%: Although the growth in orders is lower than the increase in sessions, it shows that a substantial portion of the increased traffic is converting into purchases.

•Demand Increased +4.66%: The increase in demand is a positive sign for Tier 2 brands.

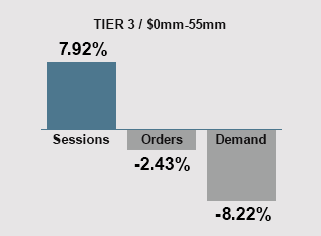

Tier 3 Brands

•Sessions Increased +7.92%: Tier 3 brands saw sessions increase.

•Orders Decreased -2.43%: Despite higher session volumes, orders were down compared to last July.

•Demand Declined -8.22%: Declines in demand reflect broader market trends, with consumers tightening their budgets or prioritizing essential goods over discretionary spending. Brands may need to reconsider their product offerings, pricing strategies, and promotional efforts to align better with consumer needs and behaviors.

GET IN TOUCH

Questions? Need help integrating online and offline channels?

Tags: June 2024 Marketing Benchmarks, June 2024 Marketing KPIs