We compiled these trends from over 100 brands, comparing year-over-year data for the date range April 1, 2024, to April 30, 2024.

April 2024: Spring Softness Continues

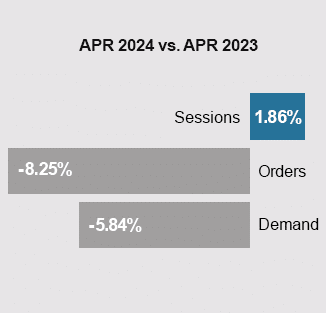

Following a sluggish trend, shopper activity remained subdued in April. Although demand for apparel remained robust, other sectors experienced declines compared to the previous year.

Despite economic challenges such as inflation, consumer engagement persists, contributing to our optimistic outlook for 2024. While the economy is expected to slow in the upcoming months, steady growth is still anticipated throughout the year.

The National Retail Federation predicts retail sales will increase 2.5% to 3.5% in 2024, signaling a return to pre-pandemic growth levels. Monitoring this trend closely, especially as we transition into Q2, will be crucial.

April 2024 Marketing Trends

Trend #1: Consumer Spending and Well Being Outlook

Spending intentions have remained subdued due to a renewed focus on savings, prolonged inflation effects, and consumer hesitance towards high prices. The financial well-being of Americans has evolved since the pandemic’s onset, initially boosted by government stimulus and savings, then declining as inflation rose. However, it has since recovered, aided by easing inflation and rising real earnings. Additionally, the traditional “lipstick index” may not fully capture the breadth of splurge purchases across diverse categories like food, beverages, and electronics, driven by hedonic and practical motives. This behavior reflects individuals indulging in small, affordable luxuries to uplift their spirits during economic challenges. Understanding these motivations can assist retailers in tailoring effective marketing strategies.

Moreover, the National Retail Federation anticipates a modest growth in retail sales of 2.5% to 3.5% in 2024, in line with pre-pandemic averages. Despite economic challenges, the economy exhibits resilience, fueled by positive consumer outlooks and robust financial health. Although job gains are projected to decelerate, consumer expenditure on goods and services is expected to increase, supported by strong consumer balance sheets and manageable debt levels. While inflation is forecasted to ease gradually, the U.S. economy is poised for modest expansion, driven by sustained consumer spending and gradual inflation mitigation.

Read more on Deloitte, Lipstick Index, National Retail Federation, & US Census Bureau

Trend #2: Google Cookie Deprecation Delayed for the Third Time

Google has again postponed the end of third-party tracking cookies in Chrome, pushing it to 2025, marking the third delay since its initial plan in 2020. Despite the intention to proceed with cookie deprecation in early 2025, Google’s decision involves collaboration with the Competition and Markets Authority (CMA) to ensure fairness. Industry insiders note uncertainty about Google’s cookie phase-out strategy despite some progress earlier in 2024. While some in the advertising sector seek clarity, regulators like the CMA are open to maintaining cookie usage.

Read more on Ad Week

Trend #3: Postal Increases Driving Some Brands to Explore Smaller Formats

Increasing postage costs, combined with the USPS announcement of more to come, has mailers searching for ways to cut costs. Many brands have already begun exploring smaller formats, e.g. gatefolds, postcards and trifolds alongside a larger catalog to replace some of their overall volumes. Others are testing smaller page counts or digest-sized catalogs which can mail at a letter rate, while maintaining the proactive touch that sets physical marketing apart from digital.

Other brands have leveraged digital catalogs to minimize production costs while giving consumers an interactive tool to experience the brand.

Read more on the J.Schmid blog here

Trend #4: Apple’s New iPad Commercial Stirs Criticism Around Technology Replacing Creativity

Apple released their new iPad, and the commercial has stirred controversy. The ad shows creative instruments (piano, record player, books, paint, etc) being crushed by the new iPad. Actor Hugh Grant tweeted @tim_cook, “The destruction of the human experience. Courtesy of Silicon Valley.”

“My initial thought was that Apple has become exactly what it never wanted to be,” Vann Graves, executive director of the Virginia Commonwealth University’s Brandcenter, said.

Graves pointed out the contrast to Apple’s famous 1984 ad, which he said focused more on uplifting creativity and breaking out of the box. In contrast, Graves added, “this (new iPad) commercial says, ‘No, we’re going to take all the creativity in the world and use a hydraulic press to push it down into one device that everyone uses.’”

Apple has since apologized for missing the mark with this commercial and it will no longer be aired.

Read more on AP News here

Jump to Section

Marketing KPIs: April 2024 Trends by Industry

Marketing KPIs: April 2024 Trends by Company Revenue

$100M+ | $15M-$100M | $0-$15M

Marketing KPIs: April 2024 Trends by Industry

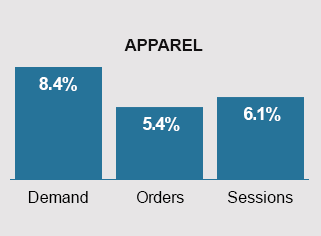

Apparel Growth Continues

•Demand Increased +8.4%: Demand growth exceeded the rise in orders and sessions for April. Apparel brands continue to experience notable increases in demand, largely attributable to their effective strategies of raising prices and achieving higher average order values.

•Orders Increased +5.4%: High conversion rates in April suggest that consumers are gearing up for the upcoming warmer months.

•Sessions Increased +6.1%: The increase in web traffic reflects enduring consumer interest in apparel, further amplified by effective marketing strategies that enhance engagement.

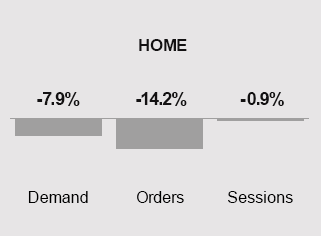

Home Brands Experience Decline

•Demand Decreased -7.9%: Despite the substantial decline in orders for Home retailers, the high average order values helped mitigate the impact, resulting in demand down slightly to last April.

•Orders Decreased -14.2%: The notable decrease in orders may reflect shifts in consumer behavior. Consumers are prioritizing essential needs over leisure spending, impacting sales of non-essential items

•Sessions Decreased -0.9%: The slight decrease in sessions suggests a decline in customer engagement. Moving forward, home brands should focus on enhancing their acquisition efforts in the upcoming months leading up to Fall/Holiday.

Specialty Retailers Commanding Higher Prices

•Demand Decreased -12.3%: The considerable decline in orders for specialty retailers was somewhat mitigated by high average order values, resulting in demand remaining down to last April.

•Orders Decreased -16.3%: The drop in orders suggests changing consumer priorities. Many are prioritizing essential needs over leisure spending, impacting sales of non-essential items

•Sessions Decreased -10.9%: Sessions for specialty brands experienced a notable decline compared to April last year. Improvements in acquisition and retention strategies are expected to yield positive results, particularly with sustained high average order values.

Marketing KPIs: April 2024 Trends by Company Revenue

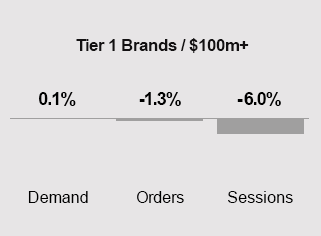

Tier 1 Brands: Remain Flat

•Demand Flat +0.1%: Year-over-year, sessions have experienced a slight decline. Tier 1 brands could potentially enhance their performance by exploring additional acquisition strategies.

•Orders Decreased -1.3%: In April, a slight decrease in orders impacted conversion rates, indicating minimal growth despite a drop in sessions.

•Sessions Dropped -6.0%: Year over year, sessions have slightly decreased. Tier 1 brands could consider exploring additional acquisition strategies to counter this trend.

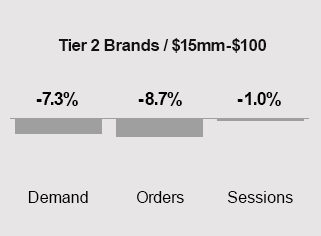

Tier 2 Brands: High Engagement, Low Conversions

•Demand Decreased -7.3%: Tier 2 brands experienced a decline in demand compared to the previous year, indicating reduced overall customer spending.

•Orders Down -8.7%: Conversion rates dropped this April. Since sessions remained flat, brands might want to explore additional browse or cart abandoned retargeting programs.

•Sessions Flat -1.0%: In April, traffic levels stayed consistent for several Tier 2 brands. It’s essential to prioritize monitoring customer engagement and enhancing acquisition efforts in the upcoming months.

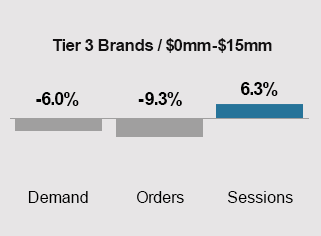

Tier 3 Brands: Conversion Challenges

•Demand Decreased -6.0%: Tier 3 brands experienced decreased demand compared to the previous April. Consumers continue to express worries about rising prices and the effects of inflation.

•Orders Decreased -9.3%: Conversion rates declined compared to the previous year. Given the rise in sessions, brands should explore the potential benefits of implementing additional retargeting programs for browsing or cart abandonment.

•Sessions Increased +6.3%: The surge in sessions reflects heightened customer engagement. However, although more individuals are browsing, the decrease in demand and orders indicates fewer are completing purchases. Tier 3 Brands face significant conversion challenges that need attention.

In the News

Digital Velocity Podcast

Barbara Turley joins Tim and Erik for an in-depth conversation on opportunities of utilizing virtual assistants to help navigate the challenges of scaling a business.

Midland Carbon Balanced Paper

Midland, a proud partner of the World Land Trust-US and Carbon Balanced Paper North America, is ready to guide you through an effortless journey. Achieve your carbon reduction targets seamlessly, while maintaining your current paper or packaging grades. We’re here to help!

⇨ Brand Loyalty: The Goal

As marketers, our mission is to attract buyers and drive sales. But the real prize is loyalty. How do we transform customers into brand advocates? To cultivate brand loyalty, let’s rethink marketing, branding, and customer experience.

US Ad Spend Expansion

In March, the U.S. ad market marked its 11th straight month of growth, expanding by 4.3% compared to March 2023. While the top 10 categories saw a modest spending increase of 1.9% over the previous year, all other categories surged by 7.9%. This growth was fueled by a significant rise in digital ad spending, up by 15.7%, while traditional media experienced a decline of 13.6% year-over-year.

GET IN TOUCH

Questions? Need help integrating online and offline channels?

Tags: March 2024 Benchmarks, March 2024 KPI, March 2024 Marketing Trends